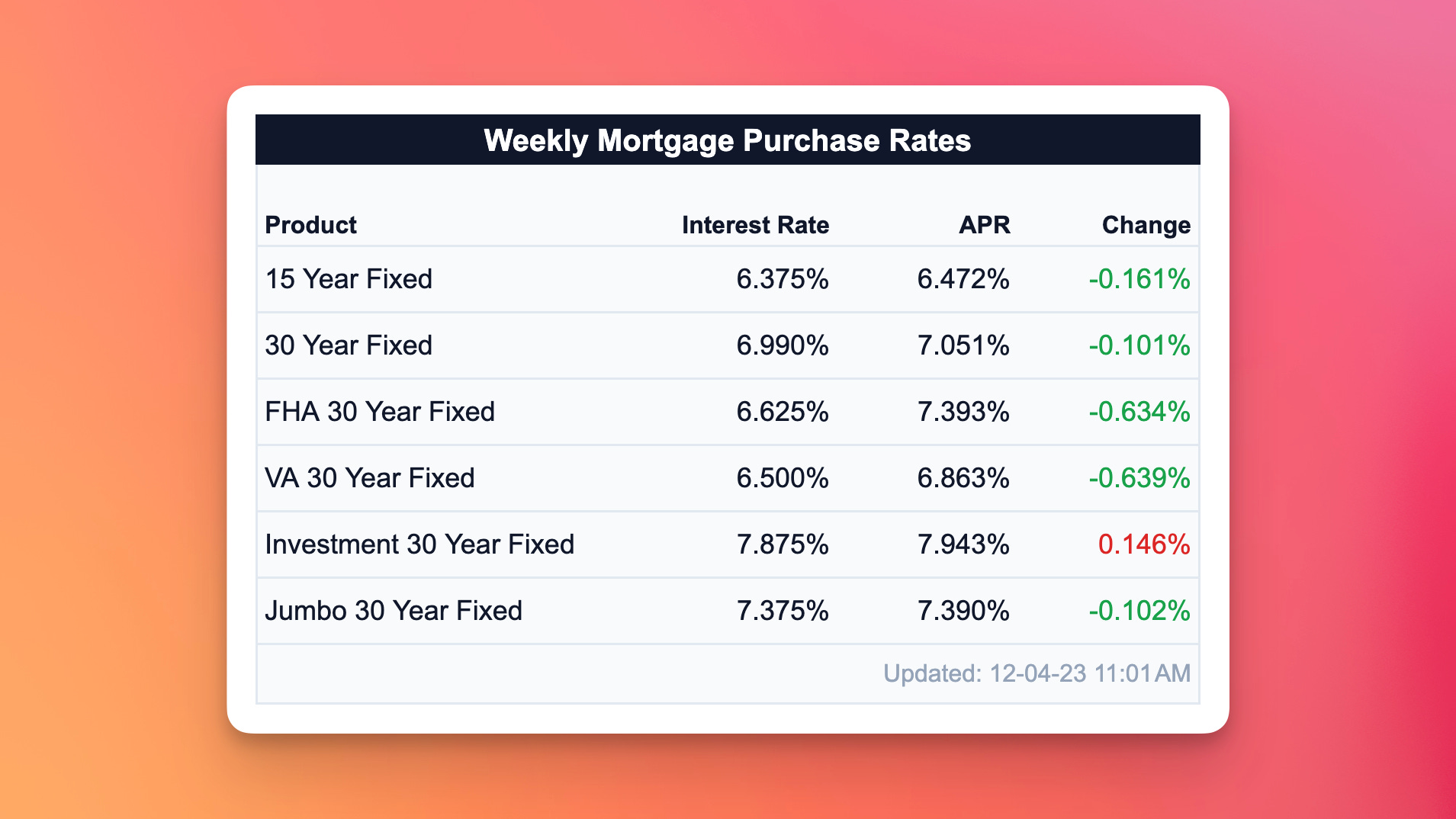

Rates Dip, Fed Hints Change - Dec 4 - Weekly Mortgage Update

Federal Reserve hints at potential rate cuts, sparking a dip in mortgage rates amid mixed economic signals.

Purchase or Refinance Quotes

A complete workup of your payment and closing costs on any home purchase or existing mortgage refinance. (same-day response, no credit check required)

⭐️ Check This Out

Mortgage delinquencies are at 2.8%, proving that avocado toast isn’t all that expensive after all. The record is 0.9% in 1999, the year before all computers were supposed to go on a Y2K strike.

Prepare for El Niño with energy-saving steps: lower thermostats, use natural heat, and upgrade appliances for reduced bills.

S&P CoreLogic Case-Shiller reports a 3.9% annual increase in U.S. home prices as of September 2023, continuing an upward trend.

Manchester-Nashua: still the hottest housing spot since 2021. Phoenix, meanwhile, made the biggest jump, up 114 spots to 145th.

New home sales fell by 5.6% in October - proving that the little kid in the Michael Myers mask that stares at you just a little too long does in fact, scare homebuyers too. 👀

📊 Market Update

Last week, something quite interesting happened. Usually, big economic reports are the main drivers of change, but this time, a few words from a Federal Reserve official made all the difference.

Christopher Waller, a Fed bigwig, made some comments that were music to the ears of those hoping for lower interest rates. He hinted that the Fed might be done increasing rates and even talked about conditions that could lead to rate cuts.

This was a bit of a surprise since Fed officials usually play their cards close to their chest, avoiding specific hints about future rate moves. Waller's remarks made investors think that rate cuts could start happening as soon as next May, assuming inflation keeps cooling down.

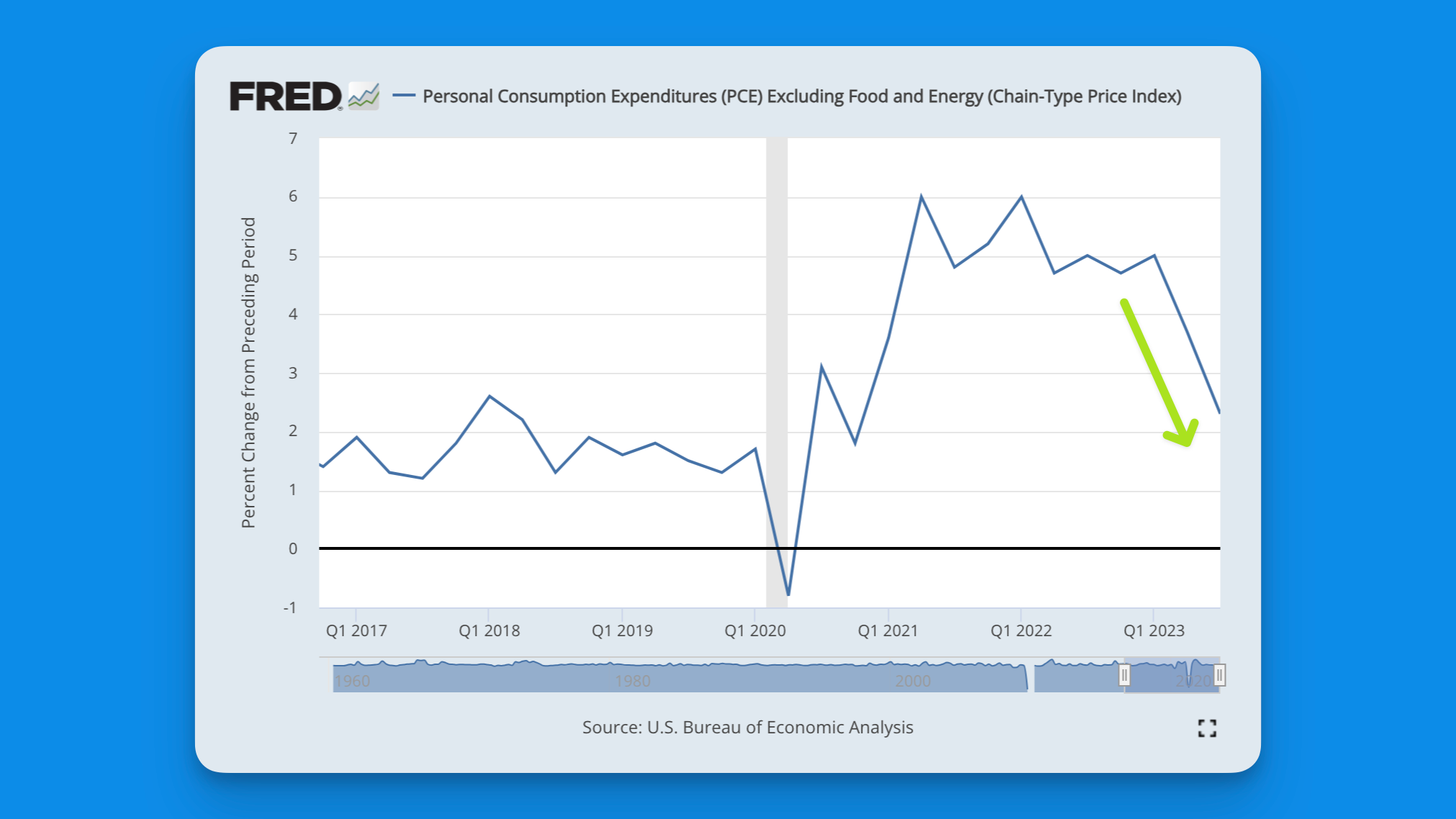

The latest inflation report showed that the core Personal Consumption Expenditures (PCE) price index – a key inflation measure the Fed watches – went up 3.5% from last year. This is still higher than the Fed's comfort zone but is the lowest since May 2021, which suggests that inflation might be on a downward trend.

Meanwhile, the manufacturing sector isn't doing too hot. The Institute of Supply Management reported that their manufacturing index is showing a contraction in the sector, the longest downward streak in about 15 years.

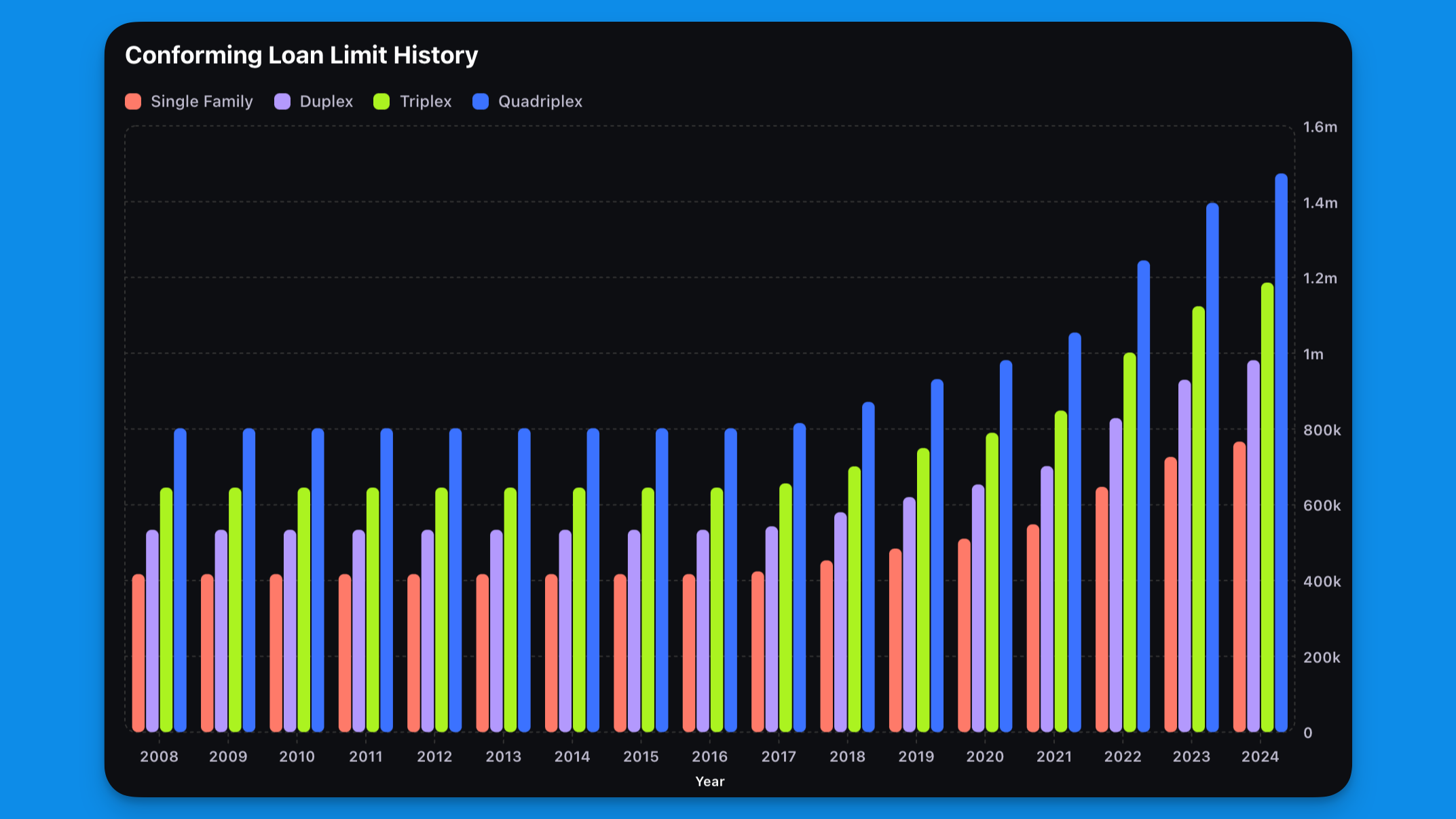

2024 Conforming Loan Limit

You'll often hear about "conforming" and "non-conforming" loans, and the difference between them is pretty straightforward. Conforming loans are basically the standard bearers; they meet specific guidelines set by Fannie Mae and Freddie Mac, two government-sponsored entities that buy and guarantee mortgages.

The most well-known guideline is the loan limit, which changes yearly. If your loan is within this limit, it's a conforming loan. On the flip side, non-conforming loans don't fit into these guidelines. The most common type of non-conforming loan is a jumbo loan, which exceeds the set conforming loan limits. These are often used to buy more expensive properties and usually come with different eligibility criteria.

In 2024, the conforming loan limit is going up by 5.5% to $766,550, and up to $1,149,825 in pricier areas (called High Cost of Living zones). This is part of a trend – it's the eighth year in a row that this limit has increased.

Later This Week

Looking ahead, everyone's eyes will be on the Fed officials for any more hints about rate changes. We're also waiting on some big reports this week, like the ISM manufacturing index, Jolts job openings data, and, most importantly, the employment reports which includes job numbers and wage info on Friday.