Rate Hikes Could Slow This Month- Dec 5 - Weekly Mortgage Update

Fed Chairman Jay Powell confirms they are considering slowing the pace of rate hikes as early as December 14th.

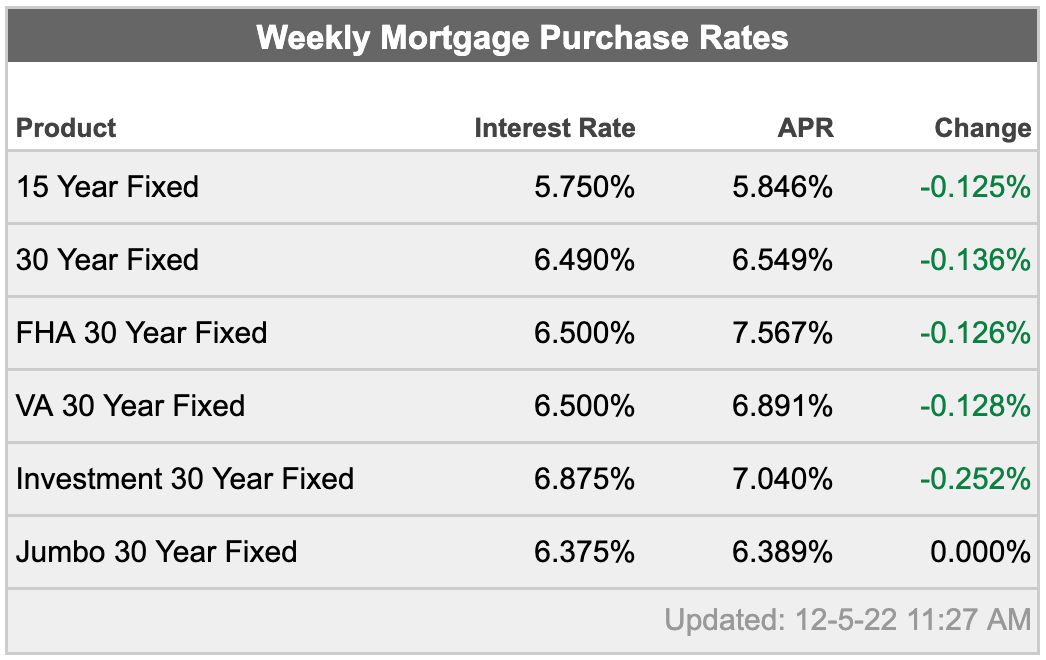

Purchase or Refinance Quotes

A complete workup of your payment and closing costs on any home purchase or existing mortgage refinance. (same-day response, no credit check required)

💵 2% New Construction Rebate

Receive up to 2% of your purchase price back at closing for closing costs. (Texas only)

⭐️ Check This Out

New home sales are up 8% month over month. It’s nice to see families snatching up the discounted inventory usually available this time of year.

Pending sales dropped 4.6% in October, but keep in mind that mortgage rates were over 7% back then. 😬 They’ve since fallen to the mid-6s.

$726,200 is the new loan limit for 2023. High-cost-of-living areas get a bump to over $1M. Check out the market update below for more details.

According to Zillow, the Midwest looks to take center stage in 2023 and be the hot market. This report goes into their top 5 predictions for the new year.

📊 Market Update

Fed Chair Powell has officially acknowledged that there has been some progress in reducing inflation. The pace of rate hikes could slow as early as December 14th.

An official announcement from the Fed Chairman is a big deal. Last week’s report clued us in that they were considering it from the monthly meeting minutes that were released. Now that we have an official statement, investors expect a 50 basis point hike instead of the usual 75.

Does a Fed rate increase mean higher mortgage rates?

Not necessarily. There’s one key thing to remember about the Fed vs. the market.

The Fed is backward-looking

The market is forward-looking

As a result, the market is always trying to predict the Fed’s next move. Here’s what I generally expect when it comes to short-term, future mortgage rates:

If the Fed does what it says it will do, mortgage rates stay around the same

📈 If the Fed surprises the market with a hawkish statement, I expect a spike in mortgage rates

📉 If the Fed surprises the market with a dovish statement, I expect a dip in mortgage rates

A Pop Quiz! On a Monday!

Let’s test whether you notice the differences between Fed sentiments. Which one of these comments is dovish, and which one is hawkish?

"The Fed needs to take proactive steps to continue to raise interest rates in order to keep inflation in check."

"Given the uncertain economic outlook, the Federal Reserve stands ready to provide additional accommodation if needed to support the recovery."

Notice the difference? You're correct if you guessed that the first is hawkish and the second one was dovish. Two points for Gryffindor!

Hawkish is generally bad for mortgage rates. Dovish is what you’re looking for to see lower mortgage rates.

FHFA Announces New Loan Limits

The FHFA (Federal Housing Finance Agency) has announced that the conforming loan limit for Fannie Mae and Freddie Mac mortgages in 2023 will increase by 12% to $726,200 and 150% to $1,089,300 in most high-cost areas, marking the seventh consecutive year of increases.

What is the difference between a conforming and a non-conforming loan?

Conforming Loan

Starting in 2023, any loan that is $726,200 or lower

Generally easier to qualify for than non-conforming loans

Requires as little as 3% down to qualify

Non-Conforming Loan (also called a “Jumbo Loan”)

Starting in 2023, any loan of more than $726,200

Generally more challenging to qualify for than conforming loans

Usually requires 20% down or more to qualify (in some cases, there are programs available with 10-15% down)

Currently, jumbo loan interest rates are generally lower than non-jumbo loans. This isn’t always the case, so it’s always best to get a quote to know what to expect ahead of time.

🗓️ This Week

Monday (today) - ISM national services - an indicator of the overall economic condition for the non-manufacturing sector.

Thursday - Initial Jobless Claims - measures the number of individuals who filed for unemployment insurance for the first time during the past week.

Friday - Core PPI - measures the change in producers' selling price of goods and services, excluding food and energy.