Fed Week - Jan 30 - Weekly Mortgage Update

Last week was unsurprisingly calm, as the Federal Reserve is currently in its blackout period leading up to their meeting.

Purchase or Refinance Quotes

A complete workup of your payment and closing costs on any home purchase or existing mortgage refinance. (same-day response, no credit check required)

⭐️ Check This Out

Sellers surrender and bend to the will of the buyers, as 42% of them generously offered bribes (aka concessions) in the form of repairs, credits, and rate buydowns in Q4 of 2022.

The average American is content with a 716 FICO score, but getting past 800 isn’t all that difficult. This CNBC article details how anyone can attain it without making a blood pact with Equifax.

The streak continues as existing home sales decline for 11 consecutive months, but hey, it's not all bad news - a 1.5% decrease in MoM sales beats November's 7.7% nosedive, and there's a slight improvement in the annualized sales pace.

The Real Estate Confidence Index for January shows a rise in first-time buyers (31%) due to lower mortgage rates and more affordable prices. Meanwhile, agents continue to witness lawn dance battles, with listings getting more than 2 bids on average.

📊 Market Update

Last week was unsurprisingly calm, as the Federal Reserve is currently in its blackout period leading up to their meeting. The next meeting is on Wednesday, where the Fed is expected to announce a 25 basis point rate increase.

The Blackout Period

The Federal Reserve "Blackout Period" refers to the 12 days before a Federal Open Market Committee (FOMC) meeting, during which Federal Reserve officials are restricted from making public comments or speeches about monetary policy.

Fed governor commentary tends to cause market volatility (for better or worse), so any time they are forced to zip it, we usually get a bit of a reprieve from the major swings we’ve come to expect.

Core PCE, GDP, and Housing

The Core PCE (that's Personal Consumption Expenditures to you and me) is up 4.4% from a year ago, which matches expectations but is still higher than the Fed's target level of 2%. Meanwhile, the 4th quarter GDP came in at 2.9%, which is above forecast, but it's the third quarter in a row that it's dropped, and it's projected to continue weakening.

On the bright side, consumer and government spending is still looking strong. However, the housing market is facing some challenges, as new home sales dropped 16% in 2022 compared to 2021. The median home price is now $442,100, up 8% from last December.

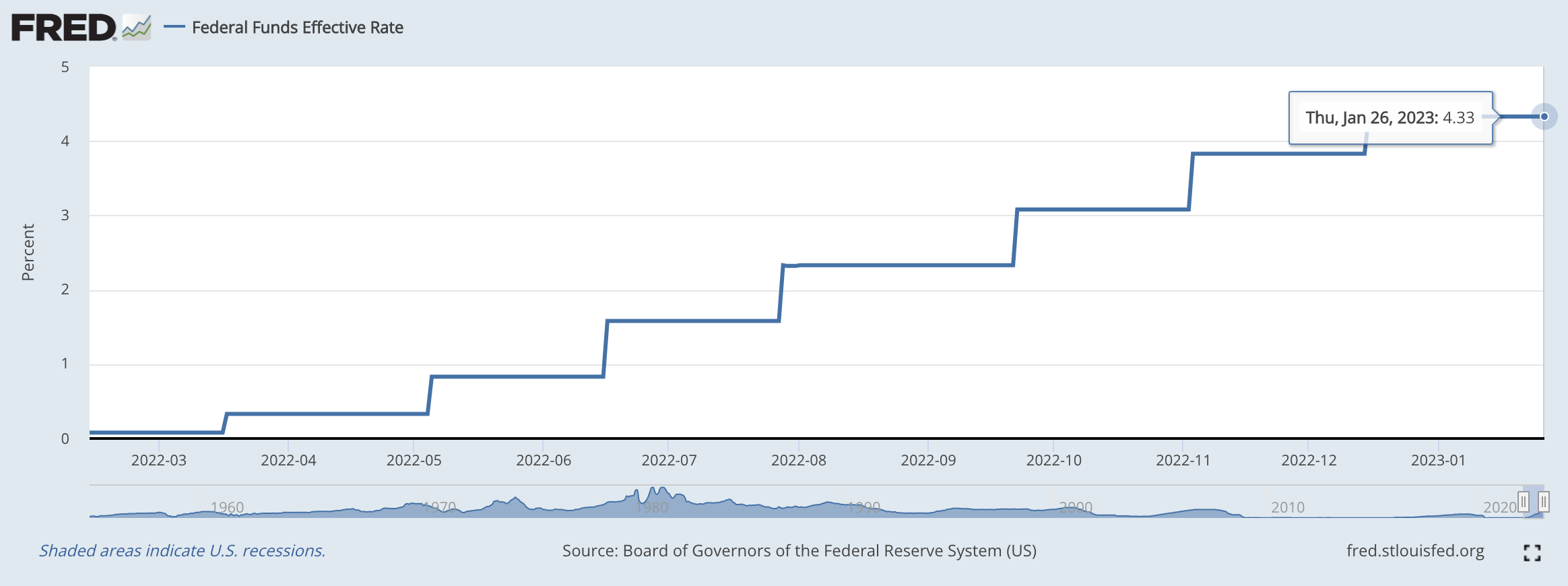

Fed Meets This Wednesday

The need to lower inflation by increasing the target Federal funds rate has been going on since March 2022. Each rise in the chart above coincides with an announcement by the Fed (like the one expected this week) to raise their target rate higher.

A rise in the Federal Funds rate, the interest rate at which banks lend to each other overnight, typically has a ripple effect throughout the financial and mortgage markets.

In the financial market, we’ve seen:

An increased cost of borrowing, making it more expensive for consumers and businesses to take out loans.

A decline in stock prices as investors adjust to the higher cost of borrowing.

A strengthening US dollar as investors look for safe-haven assets in response to higher interest rates.

In the mortgage market, we’ve seen:

An increase in mortgage rates - one of the most rapid increases on record.

A reduction in demand for homes and a slowing of the housing market.

We’re nearing the end of the projected rate hikes until we eventually see the Fed “pause” for some time. The market expects the pause to end and pivot to follow before current projections and by the end of 2023.

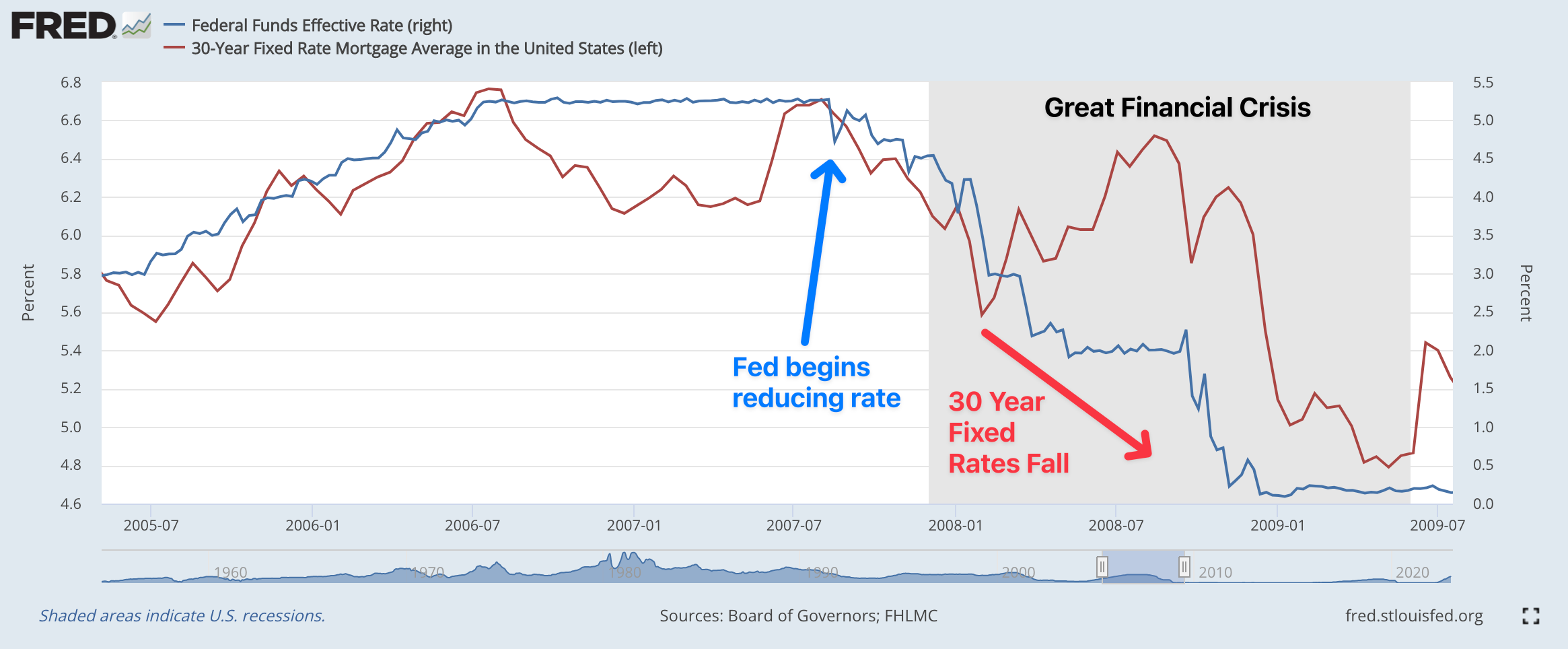

The Last Fed Pivot

During the last series of Fed rate hikes before 2008, until the eventual collapse of the US housing market, mortgage rates trended higher with the Fed target rate. The average 30-year fixed rate peaked near 6.875%, and bottomed at 4.750%; over a 2% change over a year and a half.

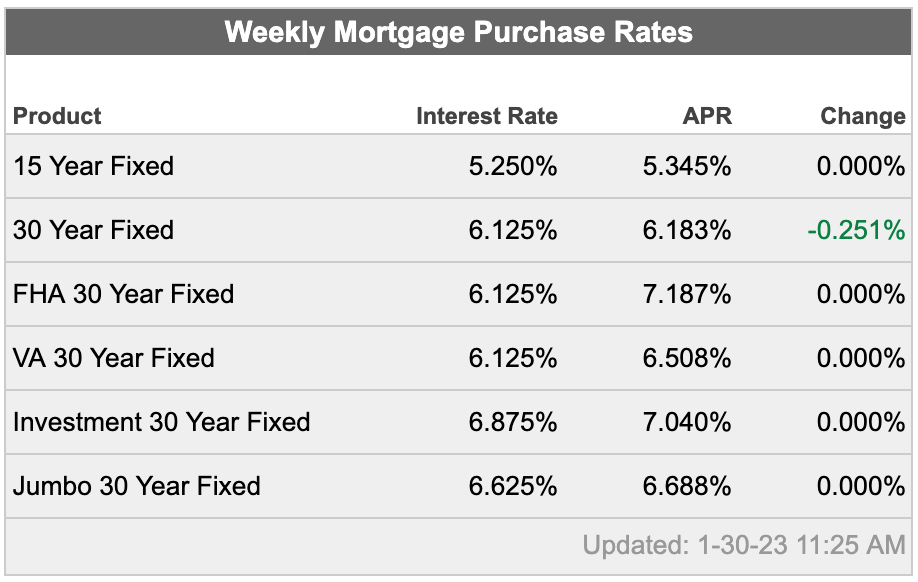

Today, the average 30-year fixed rate is 6.125%. If we were to see the same type of regression in mortgage rates after the Fed pivot, you could expect to see 4.125% again by the end of 2025 - mid-2026, assuming the Fed pivots at the end of this year.

As a result, one could assume that any mortgage obtained this year will likely be refinanced within 2 years if history repeats itself.

🗓️ Economic Calendar

Economic data drives mortgage interest rate movements, so it's important to keep an eye on these events. Here are the key economic events for this week.

Wednesday

FOMC Statement - the official announcement from the Fed and interest rate decision. The market expects a 25 basis point hike.

Friday

Employment Reports - Earnings, unemployment rate, and wage inflation numbers are released. The forecast vs. actual tends to increase market volatility.